When accounting firms notice the first sign of a cybersecurity incident, it could already be too late. From a locked system to missing files and suspicious transactions, even a minor breach can ripple across dozens or hundreds of clients. With digital financial data becoming a core part of many operations, accounting companies cannot afford to operate without an incident response plan.

Why Accounting Firms Are Prime Targets for Cyberattacks

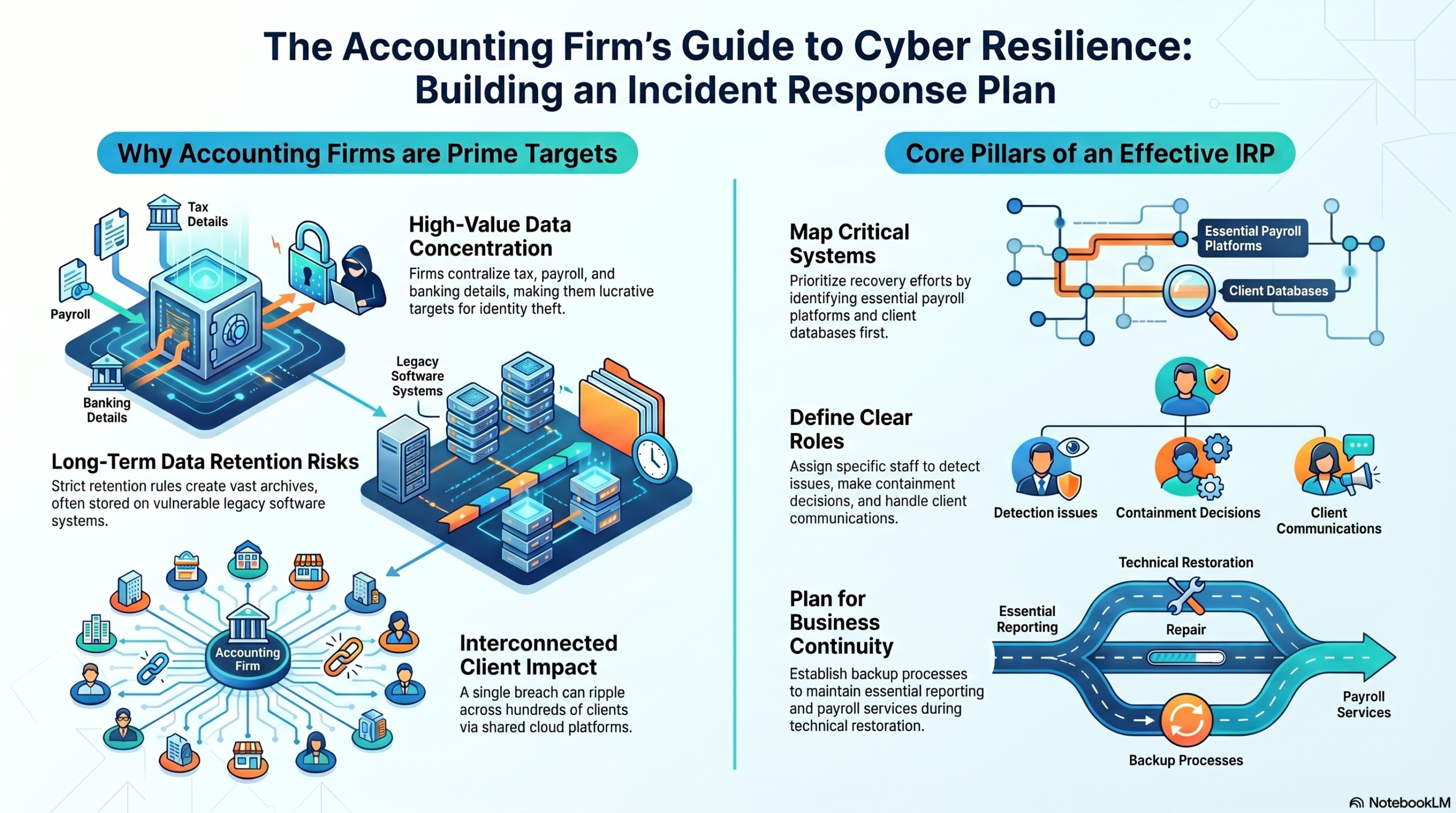

Accounting firms handle sensitive financial information as part of their daily operations, making them a prime target for cyber attackers. To gain access to this information, attackers deploy common methods such as phishing, ransomware and data breaches. The way firms manage and retain this data also creates conditions that make these attacks more effective.

High-value data concentration

Cybercriminals target accounting firms because they provide a concentrated source of sensitive financial and personal information. The information is often complete enough to support identity theft and financial fraud, making these systems particularly lucrative targets. As accounting systems typically store tax records, payroll data and banking details in a single location, this centralized storage increases the risk of a successful breach.

Long-term data retention

Strict retention rules require firms to store financial records for long periods. While necessary, this creates extensive data archives that may not always receive the same level of protection as active systems. For instance, older software and legacy storage systems can become vulnerable points that attract attackers’ attention.

The Importance of an Incident Response Plan

An incident response plan is a critical component of cybersecurity preparedness for accounting firms. It defines how an organization responds when a cyber incident occurs, helping to reduce damage and speed up recovery.

Maintaining control across client systems

Accounting firms often operate across multiple client environments, including serving as outsourced accounting specialists to deliver specific services. To ensure efficiency, they may rely on cloud-based systems and digital tools to manage financial data for multiple clients within a single platform, creating a highly interconnected environment. An incident response plan provides a structured framework for responding to cyber incidents, reducing the impact across interconnected client systems.

Speeding up response and reducing disruptions

A well-defined response plan ensures that in-house teams can promptly identify and isolate affected systems, preventing malware from spreading further across the company’s internal networks. Early intervention allows technical teams to begin recovery processes sooner, reducing downtime and further disruptions to the business’s operations.

Supporting compliance and regulatory requirements

An effective plan helps firms meet regulatory and legal obligations surrounding data breaches. It can reduce penalties and support compliance during audits or investigations. For example, the Gramm-Leach-Bliley Act requires financial firms to safeguard clients’ financial information. Having a documented incident response process shows that the firm has taken reasonable steps to protect sensitive information.

How to Create an Effective IRP

Creating an effective incident response plan requires careful planning. The plan should be practical and easy to follow in real time during a cybersecurity incident.

Identify critical systems first

Firms should map out which systems are essential for daily operations, such as payroll platforms, client databases, tax filing tools, and other sensitive information. Understanding what is important ensures teams can prioritize recovery efforts correctly during an incident.

Define clear roles

Every team member should know exactly what they are responsible for during a cyber incident. Allocation of roles includes who detects and reports issues, who makes containment decisions and who communicates with clients.

Test and update the plan regularly

The incident response plan needs to be up to date. Whenever any systems or processes change, the internal team must ensure the plan remains relevant. From time to time, holding regular simulation sessions and training exercises helps staff stay familiar with procedures and highlight weaknesses in the plan.

Plan for business recovery and continuity

Beyond containment and recovery of systems, firms must also plan for how core services will continue during disruption. It includes identifying backup processes and potential outsourced support to maintain essential functions such as payroll and reporting. A strong recovery strategy ensures the firm can continue serving clients even while technical teams restore systems, reducing the financial impact and preserving trust.

Staying Prepared

Incident response planning is no longer optional for accounting firms operating in a digital environment. Cyber threats continue to grow in complexity, making preparation essential for protecting sensitive financial data. By investing in preparedness, firms can effectively strengthen resilience and safeguard both clients and business stability.

As the Features Editor at ReHack, Zac Amos writes about cybersecurity, artificial intelligence, and other tech topics. He is a frequent contributor to Brilliance Security Magazine.

.

.

Additional Resource

Video Overview

Follow Brilliance Security Magazine on LinkedIn to ensure you receive alerts for the most up-to-date security and cybersecurity news and information. BSM is cited as one of Feedspot’s top 10 cybersecurity magazines.